Start Your Custom Quote Process™

Our partners

Table of Contents

- Medical Liability Claims Trends for New Mexico Healthcare Providers

- How to buy medical malpractice insurance in New Mexico.

- How to save money on your malpractice insurance.

- How much does medical malpractice insurance cost in New Mexico?

- Medical malpractice requirements in New Mexico.

- Find Coverage for your Practice

- Client Testimonials

- Best medical malpractice insurance companies in New Mexico.

- Why partner with Cunningham Group in New Mexico?

- Historic medical malpractice insurance rates in New Mexico – since 2000.

- History of malpractice insurance in New Mexico.

- New Mexico Patient Compensation Fund.

- Resources for Physicians.

New Mexico Malpractice Insurance

New Mexico premiums are lower than in most states. New Mexico is one of only seven states with a Patient Compensation Fund (PCF), and the state has a $600,000 cap on total damages (excluding punitive damages and past and future medical care).

Our Physician Buyers Guide for purchasing malpractice insurance in New Mexico gives you the information necessary to obtain the strongest, most financially secure policy at the best price. When shopping for coverage, you need a full view of the New Mexico marketplace to find the company that best fits your situation. Choose a broker that can offer multiple quotes from all the major malpractice insurance companies in New Mexico.

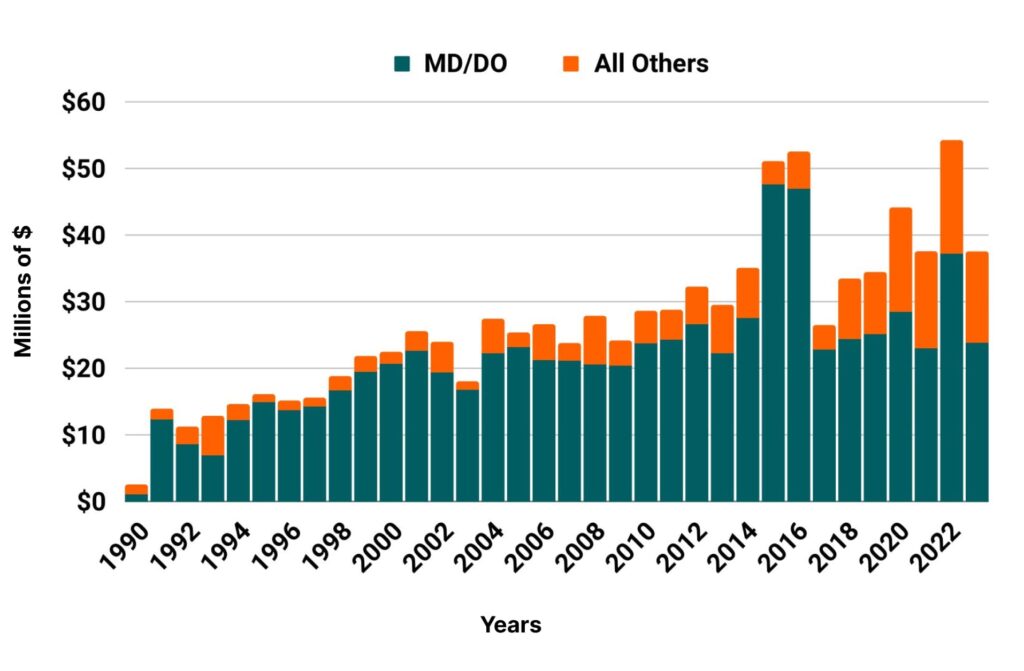

Medical Liability Claims Trends for New Mexico Healthcare Providers

New Mexico NPDB from 1990 to 2023

How to buy malpractice insurance in New Mexico.

The best way to buy malpractice coverage is to work with a reputable malpractice insurance broker in New Mexico who can generate multiple quotes. Your broker will walk you through the lengthy insurance application and underwriting process. Click to get medical malpractice insurance quotes from every major New Mexico malpractice insurance company.

Typically, the malpractice insurance purchasing process goes like this:

- Submit your information for your free medical malpractice insurance quote from every major insurance company in New Mexico.

- One of our veteran malpractice insurance agents who specializes in the New Mexico market will contact you to learn more about your specific needs.

- We shop your coverage to every major insurance company in New Mexico.

- We present you with a number of insurance quotes and give you the information necessary to make an educated and informed decision. Don’t worry. We’re here every step of the way, helping you get the best price with the best company.

- At renewal time, we restart the process of shopping your coverage among every major carrier to keep your policy properly priced.

How to save money on your malpractice insurance.

- The easiest way to save money on your medical malpractice insurance policy is by working with a broker who has the access to generate quotes from every major insurance company, offering an accurate view of the marketplace. As one of the top brokers in New Mexico, we can guide you through the application and underwriting process so you’re confident you secured the best price with the right insurer for your situation.

- The most common limits in New Mexico are $200,000/$600,000 million. Limits of liability play a major role in determining the overall cost of your policy. Some companies will offer lower limits to save you money. We don’t recommend this. We want your risks fully indemnified so you never have to pay an award out of pocket. Let us save you money by shopping your coverage rather than skimp on protection.

- Check out our 7 secrets your medical malpractice insurance agent won’t tell you page to get insider information on buying coverage in New Mexico.

How much does medical malpractice insurance cost in New Mexico.

Rates for physician malpractice insurance don’t vary much depending on where you practice within the state. Most major insurance companies classify New Mexico as a single territory, which means your specialty’s base rate does not vary depending on your practice address. But you still want multiple quotes to get an accurate view of the marketplace. This is one of the many reasons it’s important to work with an insurance agency that specializes in medical malpractice insurance. Below are mature, base rates with no credits or discounts. We typically get our clients a 30-50% reduction from these rates:

New Mexico

- Internal Medicine Average Rate $13,750

- General Surgeon Average Rate $54,538

- OB/gyn – Average Rate $74,525

Medical malpractice requirements in New Mexico.

Limits of Liability: The most common limits of liability in New Mexico are $200,000 million per claim with an annual aggregate cap of $600,000.

Most hospitals require a physician carry malpractice insurance prior to granting admitting privileges. Some of the hospital systems require this include, but are not limited to: Presbyterian Hospital in Albuquerque, CHRISTUS Saint Vincent Regional in Santa Fe and Carlsbad Medical Center.

New Mexico has a Patient Compensation Fund in place.

Client Testimonials

Below is what a few clients have to say about our prices and service. We know that cost and trust are the two most important factors when shopping for your medical malpractice insurance. We pride ourselves at being the best at both!

Best Medical malpractice insurance companies in New Mexico.

- Medical Protective

- The Doctors Company

- Preferred Professional

Why partner with Cunningham Group?

Partnering with Cunningham Group will give you a full view of the New Mexico marketplace.. Our veteran insurance agents average 10+ years of industry experience. Let us help you secure medical malpractice insurance quotes from every major insurance company in New Mexico.

Historic Medical Malpractice Insurance Rates in New Mexico for Physicians.

Brief History, about the New Mexico Excess Liability Fund and other important facts of medical malpractice insurance in New Mexico.

New Mexico is unique among states in that standard insurance carriers are only permitted to offer occurrence medical malpractice policies. Though claims-made policies are far more common nationwide, only surplus-line carriers can offer them in New Mexico. Read about the difference between claims-made and occurrence policies here.

Tort Reform in New Mexico

New Mexico first addressed its medical liability system through the New Mexico Medical Malpractice Act, passed in 1976 in response to the nationwide malpractice crisis of the 1970s. Written with input from the New Mexico Medical Society, the Act better defined the standard of care; restricted actions based on a lack of informed consent; prohibited the ad damnum clause (the section of a legal complaint specifying the dollar amount of damages); established a statute of limitations; establish a medical review commission; and limited the dollar amount of recoverable damages.

Among the most important parts of the act was the $500,000 limit on total damages, not including punitive damages and medical-care-related expenses. This amount has since been raised to $600,000. In 2011, there was an attempt to raise the cap on liability awards from $600,000 to $1 million in return for revising language that excluded medical corporations from the protections of the Medical Malpractice Act. The New Mexico Medical Board unanimously agreed to the amendments, but Gov. Susana Martinez vetoed the resulting bill because she felt the changes could lead to an increase in the number of frivolous lawsuits and cost of medical malpractice insurance.

New Mexico Patient Compensation Fund

Enacted as companion legislation to the Medical Malpractice Act, the New Mexico Professional Liability Fund Act of 1976 established a patient compensation fund. The fund is a state-established liability funding mechanisms that provides medical malpractice coverage in excess of the primary insurance requirements of the applicable state. The fund limits the amount of damages that may be awarded against an enrolled healthcare provider, thus limiting their liability and lowering medical professional liability insurance premiums. The fund is capitalized solely through surcharges (i.e. premiums) levied against its member healthcare providers. A total of six other states currently operate a patient compensation similar to New Mexico’s.

In 2017, the New Mexico Supreme Court took on the curious case of Montano v. Frezza. At the heart of the case was whether residents of New Mexico could sue Texas physician in a New Mexico court for malpractice that allegedly occurred in Texas. Thousands of rural New Mexico residents travel to Texas for medical treatment each year. Texas has arguably the strictest medical liability tort reforms in the nation, and New Mexico is generally considered a more plaintiff friendly state to pursue a medical liability claim. At risk was whether Texas physicians would continue to see New Mexican patients. The New Mexico Supreme Court ultimately decided Texas physicians could not be sued in New Mexico’s court system for healthcare rendered in Texas.

In 2018, the Second Judicial District Court in Albuquerque recently struck down a New Mexico law that caps damages in medical professional liability lawsuits at $600,000. The cap does not apply to medical expenses, but does cover compensation for things like lost wages and noneconomic, pain-and-suffering damages. Judge Victor Lopez ruled that the New Mexico Medical Malpractice Act is unconstitutional because it unjustly violates a plaintiff’s right to receive an unaltered jury verdict.

The New Mexico Supreme Court determined in 2021 that the state’s $600,000 cap on nonmedical, nonpunitive damages in medical liability lawsuits is constitutional. The New Mexico Legislature also raised the cap to $750,000 in 2021.